The New Build Fallacy: Why Shiny Doesn't Mean Smart

New builds aren’t automatically ‘safer’ investments. How Cotality’s 2025 numbers, consent cycles, and tax settings should change how NZ investors compare new stock vs value-add existing homes.

There is a particular kind of investor who confuses newness with value. They buy a brand-new townhouse off a developer’s glossy brochure, collect the keys, and call themselves a property investor. What they have actually done is pay a retail premium for a commodity product in a crowded segment — and often hand the developer margin that would otherwise be your future equity.

For years, new builds were marketed to New Zealand investors as the smart default: turnkey condition, and (for a while) more favourable interest-deductibility phasing, plus a narrative that tenants always prefer new. Sales decks are persuasive; long-run returns depend on price paid, location, and who else is selling the same product when you need to exit.

Cotality Home Value Index — calendar 2025

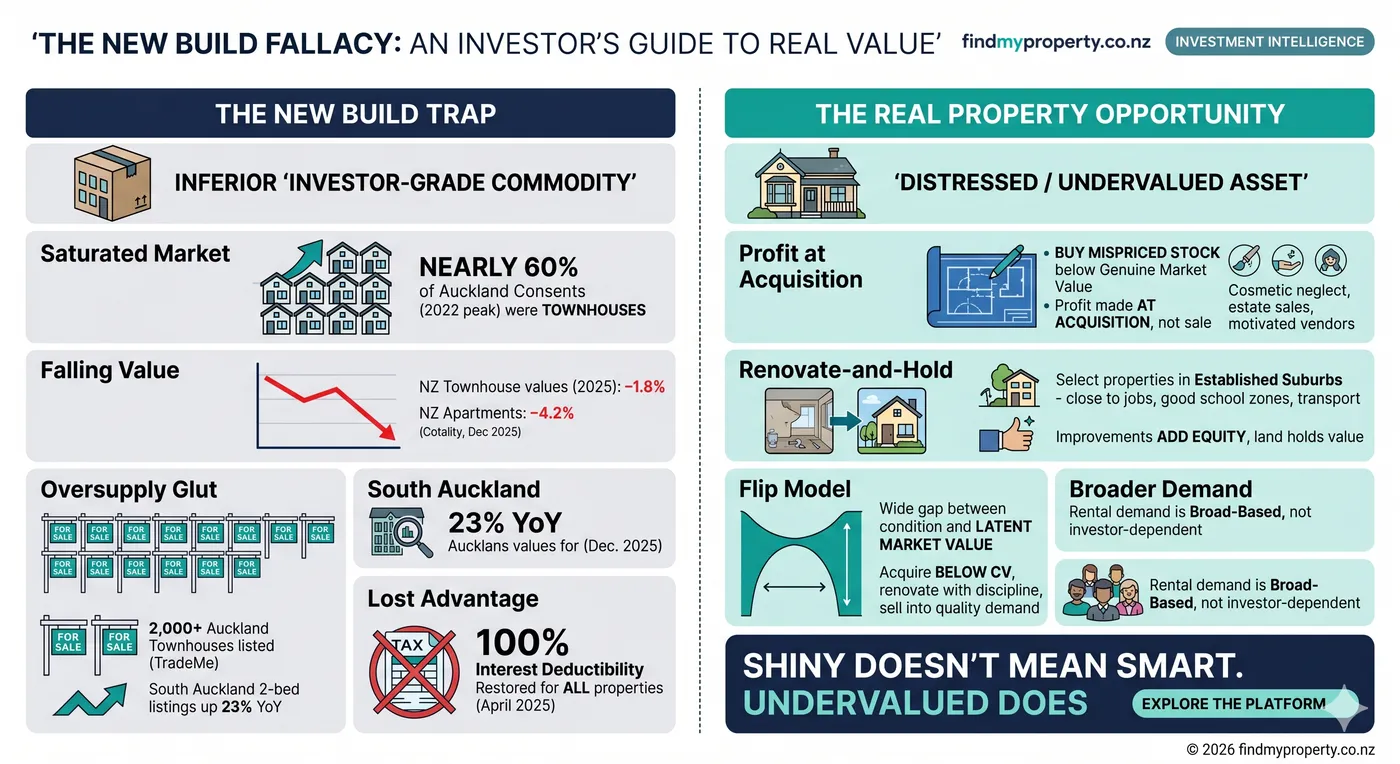

Industry reporting on Cotality’s index cited national full-year softness in 2025: townhouses about −1.8% and apartments about −4.2% (with the broad market down roughly 1%). Segment results vary by city and month — always read the latest release rather than relying on a single headline.

That context matters: when marketers still say “new is safe,” aggregate index lines for strata-style product were, at the national level, not rewarding passive holders in 2025. Auckland has been relatively weak versus parts of the country, and suburb-level results diverge widely — pockets with lots of similar new stock can see sharper softness than headline city averages when resale depth is thin.

The formula that broke

Around the consent peak (roughly 2021–2022), Auckland’s new-dwelling pipeline skewed heavily toward townhouses and apartments — industry summaries at the time noted multi-unit types making up the **majority** of activity, versus a shrinking share of standalone houses. Developers optimised for scale: repeatable two-bedroom typologies on fringe land, sold to yield-focused buyers in a low-rate world where leverage felt easy.

The model strains when the world changes: mortgages near 6%, rents that don’t keep pace everywhere, and resale buyers who compare your listing against thousands of near-identical alternatives. When owner-occupiers prefer character, space, or school zones you didn’t buy, the exit can be surprisingly thin — check the portals for townhouse inventory and days-on-market in the micro-markets you actually trade, because counts move weekly.

“Cotality has published analysis that the “new-build premium” can compress when the cycle turns. Around the GFC-era construction slump, new stock sometimes had to be discounted to clear supply — evidence that “new” is not magically insulated from repricing. Past cycles don’t predict the future, but they do puncture marketing absolutes.”

From 1 April 2025, Inland Revenue’s phased rules restore 100% interest deductibility for interest on borrowing for residential rental property, subject to the usual deductibility tests in IR’s guidance — meaning new builds no longer carry a unique, ongoing edge on interest deductibility versus existing stock.

Where the real opportunity has always been

Investors who kept their heads bought where the **gap** was widest: cosmetic distress, motivated vendors, estates, tired rental stock in strong locations — then renovated or repositioned. The thesis at FindMyProperty.co.nz is the same: economic work is largely done at acquisition, not on the exit press release. If you pay retail-plus for a mass-produced new unit, you start behind.

A well-chosen existing home near real jobs, schools, and transport often holds land value better through a cycle than thin-walled investor grade product on a fringe masterplan — your mileage depends on the asset. The flip playbook is similar: buy where the uplift between “as-is” and “after” is wide, execute the works with discipline, sell into a market that pays for quality rather than brochure renders.

Put the rankings to work: Browse properties lists AI-scored stock across New Zealand; Create a free account if you want watchlists and saved views; View pricing when you’re ready to compare plans. Need a human? Contact us.

What intelligence actually looks like

Contrarian for its own sake is a gimmick; evidence isn’t. New builds are not always wrong — buying them as a blind default because “new equals safe” is the fallacy. The edge sits where perception lags reality: motivated sellers, tired stock, outdated CVs, suburbs the herd under-researched.

FindMyProperty is built to surface mispriced and high-signal listings — not the most advertised. Shiny doesn’t mean smart; undervalued, well-underwritten, does.

Disclaimer

This article is general commentary on public market themes and our product — not financial, tax, or legal advice. Verify interest deductibility and tax positions with your accountant; verify market numbers against Cotality or other primary sources before you act.

See it in action

Browse AI-scored NZ investment properties with full financial breakdowns.

Browse propertiesMore ways to get started

Plans, local team contact, and background on who builds FindMyProperty.

More Articles

Best Bang-for-Buck Renovations for NZ Property Investors (2026)

Which NZ renovations actually return $2 for every $1 spent? Bedroom conversions, kitchens, bathrooms, cosmetic refreshes, and the structural traps that destroy flip ROI — with real NZ case studies and a pre-renovation checklist.

Read →🗺️Where to Buy Investment Property in June 2026

A data-backed breakdown of every major NZ investment region — median prices, gross yields, HPI performance, tax and rate backdrop, and who each market actually suits in mid-2026.

Read →