The Quiet Upswing: NZ Regional Property Markets in April 2026

National averages hide a split market. Election-year noise, OCR headlines, and flat index prints can mask regional strength. A fact-grounded read for NZ property investors, plus how to stress-test listings on FindMyProperty.

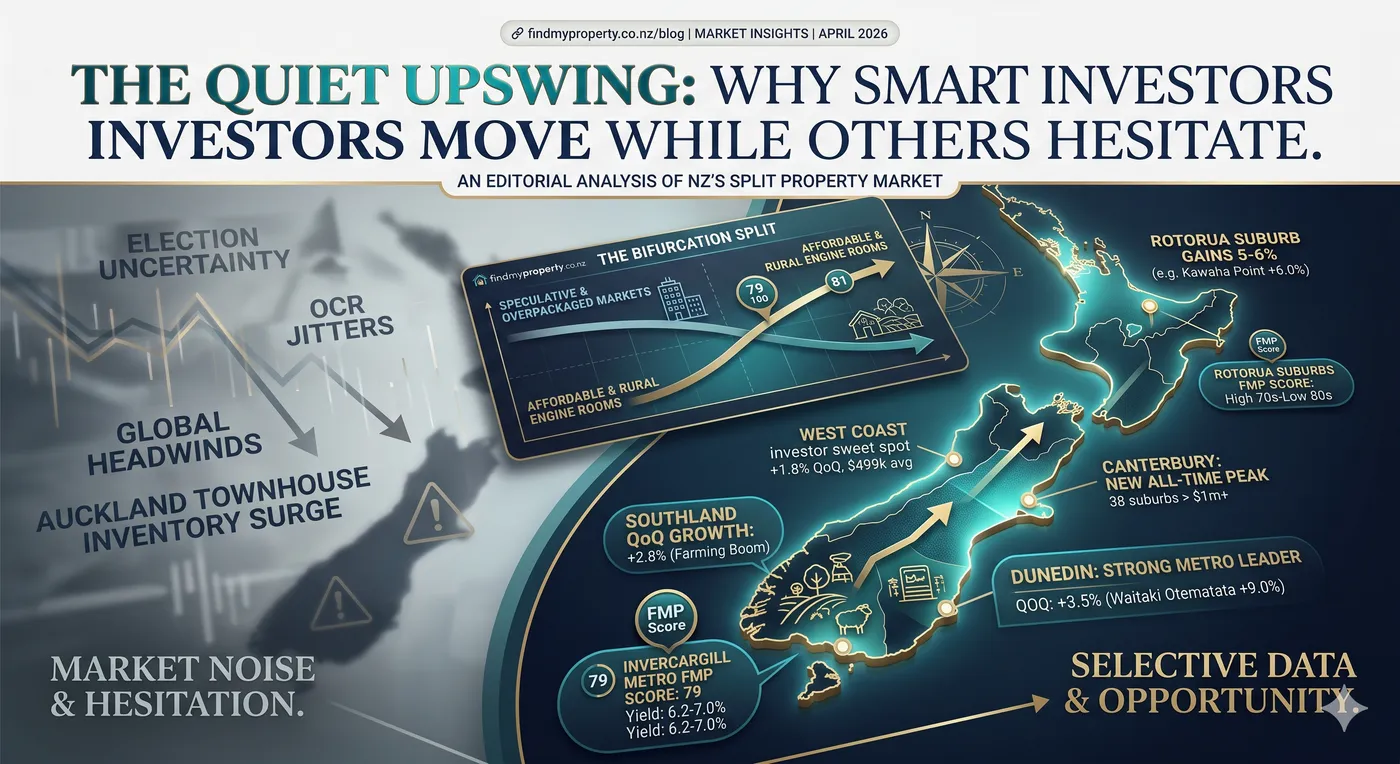

Read the split, not the slogan

When headline indices look dull, the real story is often regional. April 2026 is a useful reminder: treat national averages as a summary line, not a purchase decision.

Every cycle has moments where the dominant narrative and the on-the-ground data disagree. In New Zealand property, that gap is easy to see right now: transaction counts have improved in places, listing stock is elevated in Auckland, and index providers still report only gentle national price momentum. None of that means "nothing is moving" — it usually means the market is sorting winners from laggards suburb by suburb.

This article is commentary for investors, not a forecast. It connects public index releases to a practical lens: where divergence shows up, why cashflow discipline matters in an election year, and how FindMyProperty.co.nz helps you compare listings with yield, renovation and scenario modelling before you offer.

The map is not the territory

National median lines are useful for mood — less useful for underwriting. The same month can include flat or softer parts of the North Island alongside South Island markets that have repeatedly posted more resilient reads in recent Cotality Home Value Index updates. That pattern is less "boom" than selective strength: exactly the environment that rewards buyers who compare regions, stock types, and rental maths rather than chasing headlines.

“If your decision framework starts at the national average, you will miss the suburbs where fundamentals diverge — in both directions.”

Suburb-level stories in the media can be instructive as case studies, but they are not a substitute for your own numbers. Tourism-linked towns, provincial service centres, and affordable commuter markets can all move on different drivers — employment mix, consenting pipeline, insurance and weather events, and local listing depth. Your job is to translate those drivers into rent, vacancy, maintenance, and finance assumptions you can live with.

What recent public data has emphasised

In Flip or Hold in April 2026 (published on this blog the same month) we summarised Cotality's March Home Value Index: a national median dwelling value of $802,599, a very small month-on-month lift, and values still down year-on-year — a busy but heavy market. Auckland was broadly flat in that release while Wellington softened; Christchurch and Dunedin posted modest gains. Barfoot & Thompson also reported strong March Auckland sales counts alongside elevated end-of-month listing stock — a combination that usually improves buyer choice.

| Theme | Investor takeaway (early 2026) |

|---|---|

| National index momentum | Gentle month-to-month moves can coexist with a weak year-on-year read — do not confuse quiet headlines with "no opportunity". |

| Auckland supply | Elevated stock can support negotiation — but screen carefully for apartments, body corporate costs, and insurance. |

| South Island cities | Christchurch and Dunedin have recently shown more resilience in index updates than some northern centres — still model cashflow locally. |

| Election year | Policy noise can freeze casual buyers; prepared investors focus on listings, yields, and finance pre-approval rather than punditry. |

Dead-cat bounce or something steadier?

It is reasonable to ask whether short-term strength in a pocket is a bounce after a fall. The honest answer is: sometimes. That is why we separate "price tick" from "deal quality". A better question than "is it bouncing?" is whether the purchase still works if prices are flat for another 18–24 months and if rents soften modestly. If the only way the deal succeeds is perfect timing on capital growth, you are speculating — not investing.

Where fundamentals are grounded — realistic rents, manageable vacancy, insurable assets, and a clear maintenance budget — selective buying can still make sense even when macro forecasts disagree. Major bank economists revise outlooks as inflation and employment data shift; your plan should not require any single forecast to be correct.

Election timing, the OCR, and headline noise

New Zealand's next general election is scheduled for Saturday 7 November 2026 (with advance voting from late October). Election years often increase uncertainty for households, which can slow discretionary movers — and create space for prepared investors who have finance sorted and clear criteria.

On interest rates, the Reserve Bank's Official Cash Rate path remains the anchor for mortgage pricing. Markets can reassess timing when inflation data surprises; that is normal, and it is why stress-testing repayments above today's headline rate still matters.

“Elections, OCR paths, and offshore news deserve attention — but they are inputs to risk management, not reasons to abandon a disciplined buy box.”

How FindMyProperty.co.nz fits your workflow

Our platform is built for screening and comparison: AI-assisted property scores, rental yield context, renovation estimates from listing imagery where available, and scenario tools so you can stress-test offers and hold periods. We do not publish suburb "price league tables" as investment advice — we help you turn listing-level facts into a clearer picture of risk and return before you engage a solicitor or broker.

Practical next step

Start from cashflow: if the numbers only work with aggressive rent growth or instant capital gain, keep looking. If they work on conservative assumptions, dig into insurance, body corporate, and comparable sales next.

A simple playbook for April 2026

- Buy for yield first — let capital growth be a bonus, not the entire thesis.

- Compare regions deliberately; do not let Auckland's listing depth define your view of Dunedin, Christchurch, or provincial markets.

- Treat election headlines as volatility, not a calendar for market timing — use the window to negotiate where vendors need certainty.

- Keep an eye on insurance and climate risk disclosures — they increasingly affect lending and resale liquidity.

- Use scenarios: model flat values, softer rents, and slightly higher rates before you raise your hand at auction.

See listings with scores and scenarios

Browse investment-grade analysis on live listings, then shortlist what survives your stress tests. When you are ready to talk strategy with our team, Contact us.

This article is general information only; it is not financial advice. Property investment carries risk. Always seek independent legal, tax, and financial advice before you commit. Figures referring to Cotality and agency releases reflect commentary published on FindMyProperty.co.nz in March–April 2026 and should be cross-checked against the latest provider data.

Sources

- Cotality Home Value Index commentary (as referenced in our March 2026 NZ market update on this blog)

- Barfoot & Thompson monthly residential market statistics (Auckland sales and listing stock)

- Vote NZ — 2026 General Election overview and dates

- Reserve Bank of New Zealand — Official Cash Rate and monetary policy statements

Frequently Asked Questions

Are New Zealand house prices rising everywhere in 2026?+

No. Recent index releases show gentle national momentum alongside regional differences — for example Auckland broadly flat in Cotality's March read while Christchurch and Dunedin posted modest gains. Investors should treat suburb-level fundamentals as more important than a single national line.

Does the 2026 NZ general election make it a bad time to buy an investment property?+

Election years add policy uncertainty, which can slow some parts of the market. That is not the same as "wait forever". Prepared buyers with finance in place and clear criteria can sometimes find less competition — but every deal still needs its own numbers and due diligence.

How does FindMyProperty.co.nz help with regional property research?+

You can browse scored listings, compare rental yield context, review renovation estimates derived from listing photos where available, and run scenarios on finance and hold periods — so you evaluate opportunities consistently rather than chasing headlines.

What is the difference between a market bounce and a durable investment case?+

A bounce is mostly a price chart story. A durable case includes rent that supports the mortgage in realistic conditions, manageable vacancy and maintenance, insurable risk, and a plan that still works if values stay flat for 18–24 months.

See it in action

Browse AI-scored NZ investment properties with full financial breakdowns.

Browse propertiesMore ways to get started

Plans, local team contact, and background on who builds FindMyProperty.

More Articles

Regional Property Investing Themes for NZ Investors (2026)

Five macro themes reshaping NZ regional property investment in 2026 — yield divergence, RoNS infrastructure corridors, rates and water cost squeeze, Schedule 1A granny flats, and hybrid lifestyle catchments — with REINZ May data, sources, and a practical playbook.

Read →🏠Why FindMyProperty Focuses on Sub-$750K Value-Add Renovations in New Zealand

NZ's national median sits near $775k–$808k. FindMyProperty deliberately scores renovation opportunities below $750k — forced appreciation, flip-or-hold flexibility, Healthy Homes upgrades, and housing stock quality. Here's the data-backed reasoning.

Read →